}

I’ll never forget the day my colleague Ahmad rushed into the office, visibly shaken. His father had just passed away unexpectedly, leaving his family scrambling to cover funeral expenses and outstanding debts. “I thought he had insurance,” Ahmad told me, his voice breaking. It turned out his father’s term life policy had expired two years earlier, and he hadn’t renewed it. This heartbreaking situation opened my eyes to how crucial it is to understand not just if you have life insurance, but what type you have. The term vs whole life insurance in Malaysia debate isn’t just about numbers and policies—it’s about protecting the people you love most.

If you’re reading this in 2026, you’re likely facing the same question thousands of Malaysians grapple with every year: Should I choose term life insurance or whole life insurance? Both options promise to protect your family, but they work in fundamentally different ways. The choice you make today could impact your family’s financial security for decades to come.

Key Takeaways

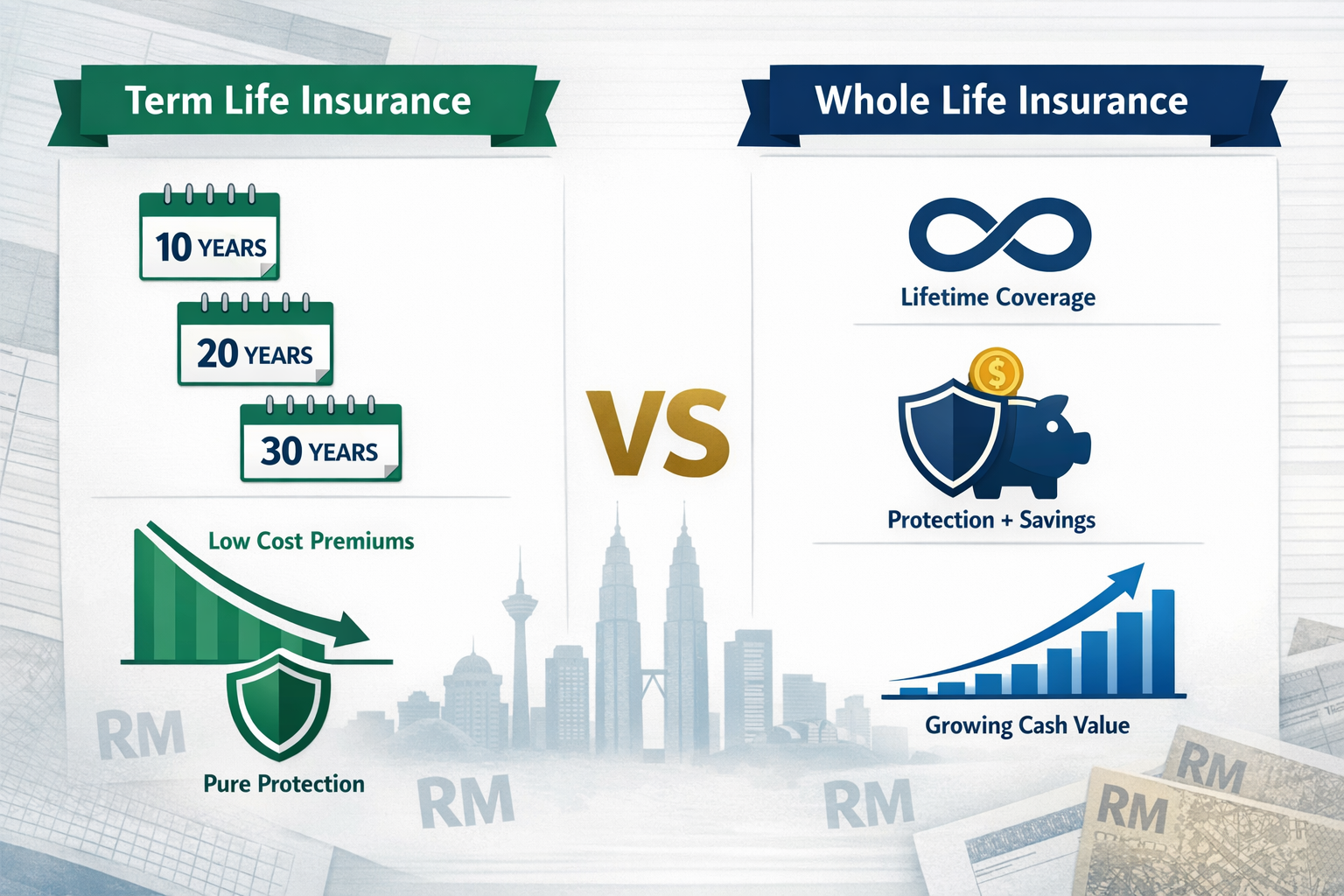

Term life insurance provides pure protection for a specific period (10-30 years) at significantly lower premiums, making it ideal for young families and those with temporary financial obligations like mortgages or children’s education.

Whole life insurance offers lifetime coverage with a built-in savings component that accumulates cash value, functioning as both protection and a long-term investment tool, though at substantially higher premium costs.

The “better” choice depends entirely on your personal circumstances: your age, income, financial goals, dependents, and whether you prioritize maximum coverage affordability or lifetime protection with wealth accumulation.

Most Malaysians benefit from term insurance when they need the most coverage during their working years, while whole life insurance suits those seeking permanent protection and a forced savings mechanism.

You don’t have to choose just one: Many financial planners recommend a hybrid approach, combining affordable term coverage for immediate high protection needs with a smaller whole life policy for permanent coverage and estate planning.

Understanding Life Insurance Basics in Malaysia

Before we dive deep into the term vs whole life insurance in Malaysia comparison, let’s establish a foundation. Life insurance is essentially a contract between you and an insurance company. You pay regular premiums, and in return, the insurer promises to pay a lump sum (the death benefit) to your beneficiaries when you pass away.

In Malaysia, the life insurance industry is regulated by Bank Negara Malaysia (BNM) through its Insurance and Takaful framework. As of 2026, the industry has matured significantly, with over 15 licensed life insurers offering various products to suit different needs and budgets.

Why Life Insurance Matters for Malaysians

According to the Life Insurance Association of Malaysia (LIAM), the insurance penetration rate in Malaysia has been steadily improving, but many families remain underinsured. The average Malaysian family needs approximately 10-15 times their annual income in life insurance coverage to adequately protect their dependents.

Consider this: If you’re the primary breadwinner earning RM60,000 annually, your family would need between RM600,000 to RM900,000 in coverage to maintain their lifestyle, pay off debts, fund children’s education, and cover final expenses if something happened to you.

What is Term Life Insurance?

Term life insurance is the simplest and most straightforward form of life insurance. Think of it as pure protection—you’re essentially renting coverage for a specific period.

How Term Life Insurance Works

When you purchase a term life policy, you select:

- Coverage amount (sum assured): The death benefit your beneficiaries will receive

- Policy term: The duration of coverage (typically 10, 20, or 30 years)

- Premium payment frequency: Monthly, quarterly, or annually

If you pass away during the policy term, your beneficiaries receive the full sum assured. If you outlive the policy, the coverage simply ends, and you receive nothing back. It’s that straightforward.

Types of Term Life Insurance in Malaysia

Level Term Insurance 🛡️ The coverage amount remains constant throughout the policy term. If you buy RM500,000 in coverage, that amount stays the same whether you die in year 1 or year 20.

Decreasing Term Insurance 📉 The coverage amount decreases over time, typically aligned with decreasing financial obligations like a mortgage. As your home loan balance reduces, so does your coverage. This makes it more affordable since the insurer’s risk decreases over time.

Renewable Term Insurance 🔄 You have the option to renew your policy at the end of the term without undergoing medical underwriting again. However, premiums increase based on your age at renewal.

Convertible Term Insurance 🔀 This allows you to convert your term policy to a whole life or permanent policy without medical examination, usually within a specified conversion period.

Real-Life Example: Rashid’s Term Insurance Journey

Let me share Rashid’s story. At 30 years old, Rashid had just gotten married and taken out a RM400,000 mortgage. His wife was pregnant with their first child, and he was earning RM5,000 monthly. He needed substantial coverage but had a limited budget.

Rashid purchased a 25-year term life policy with RM500,000 coverage for approximately RM80 per month. This affordable premium gave his young family maximum protection during their most vulnerable years. By the time the policy expires when he’s 55, his mortgage will be paid off, his children will be financially independent, and he’ll have built retirement savings.

Advantages of Term Life Insurance ✅

Affordability: This is the biggest advantage. Term insurance offers the highest coverage for the lowest premium. A 35-year-old non-smoker can get RM1 million in coverage for as little as RM100-150 per month.

Simplicity: No complicated investment components or cash values to track. You know exactly what you’re paying and what your beneficiaries will receive.

Flexibility: You can tailor the coverage period to match specific financial obligations—a 20-year term for your children’s education years, or a 25-year term to match your mortgage.

Maximum Protection When You Need It Most: Young families typically need the most coverage when income is modest and responsibilities are high. Term insurance delivers this protection affordably.

Disadvantages of Term Life Insurance ❌

No Cash Value: If you outlive the policy, you receive nothing. All those premiums are gone, which some people view as “wasted money.”

Temporary Coverage: Once the term ends, you’re uninsured unless you renew (at much higher rates) or purchase a new policy (requiring medical underwriting).

Increasing Renewal Premiums: If you need to renew, premiums can skyrocket because you’re older and potentially less healthy.

No Savings Component: Unlike whole life insurance, term policies don’t build cash value you can borrow against or withdraw.

What is Whole Life Insurance?

Whole life insurance is a completely different animal. It’s permanent protection combined with a savings element—think of it as insurance plus investment wrapped into one product.

How Whole Life Insurance Works

A whole life policy provides coverage for your entire lifetime, as long as you continue paying premiums. But here’s where it gets interesting: part of your premium goes toward the death benefit, and part goes into a cash value account that grows over time.

This cash value accumulates on a tax-deferred basis and can be:

- Borrowed against for emergencies or opportunities

- Withdrawn (though this reduces your death benefit)

- Used to pay future premiums

- Left to grow and enhance the death benefit

The Guaranteed vs Non-Guaranteed Components

Malaysian whole life policies typically have two components:

Guaranteed Benefits 💰

- A guaranteed death benefit (sum assured)

- A guaranteed cash value accumulation schedule

- These are contractually promised and cannot change

Non-Guaranteed Benefits 📊

- Bonuses or dividends based on the insurer’s investment performance

- Reversionary bonuses that increase your sum assured annually

- Terminal bonuses paid when the policy matures or upon death

- These fluctuate based on the company’s performance

Real-Life Example: Siti’s Whole Life Strategy

Siti, a 28-year-old marketing executive earning RM6,500 monthly, had different priorities. She wanted lifetime protection but also struggled with disciplined saving. Her financial advisor recommended a whole life policy with RM300,000 coverage.

Her monthly premium was RM450—significantly higher than term insurance. However, Siti viewed this as forced savings. After 20 years, her policy’s cash value had grown to approximately RM85,000. When she faced an unexpected business opportunity at age 48, she borrowed RM50,000 from her policy’s cash value at favorable interest rates, without affecting her death benefit as long as she repaid the loan.

Advantages of Whole Life Insurance ✅

Lifetime Coverage: You’re covered until death, regardless of when that occurs. There’s no risk of outliving your policy.

Cash Value Accumulation: Your policy builds wealth over time that you can access during your lifetime. This serves as an emergency fund, retirement supplement, or legacy planning tool.

Forced Savings Discipline: For those who struggle to save consistently, the mandatory premium payments create a disciplined savings habit.

Estate Planning Benefits: The death benefit passes to beneficiaries tax-free in Malaysia, making it an efficient wealth transfer tool.

Premium Certainty: Your premiums remain level throughout your life (for traditional whole life policies). You won’t face shocking increases as you age.

Policy Loans: You can borrow against your cash value at competitive rates without credit checks, since you’re essentially borrowing from yourself.

Disadvantages of Whole Life Insurance ❌

Significantly Higher Premiums: Whole life insurance costs 5-10 times more than term insurance for the same death benefit. That RM80 term premium becomes RM400-800 for whole life.

Lower Returns Compared to Direct Investments: The cash value typically grows at 3-5% annually, which often underperforms direct investments in unit trusts or ETFs over the long term.

Complexity: Understanding the guaranteed versus non-guaranteed components, surrender values, and policy illustrations requires financial literacy.

Opportunity Cost: The money locked into high premiums could potentially generate higher returns if invested elsewhere and combined with cheaper term insurance.

Reduced Coverage: Because premiums are so much higher, people often buy less coverage than they actually need, leaving their families underprotected.

Term vs Whole Life Insurance in Malaysia: The Direct Comparison

Now let’s put these two options side by side and see how they stack up across the key factors that matter to Malaysian families.

Premium Comparison Table

| Age | Term Life (RM500,000, 20 years) | Whole Life (RM500,000) | Difference |

|---|---|---|---|

| 25 | RM65/month | RM380/month | 5.8x more |

| 30 | RM75/month | RM450/month | 6x more |

| 35 | RM90/month | RM550/month | 6.1x more |

| 40 | RM120/month | RM700/month | 5.8x more |

| 45 | RM180/month | RM900/month | 5x more |

Note: These are approximate figures for non-smoking males in good health. Actual premiums vary by insurer and individual health profile.

Coverage Duration 📅

Term Life Insurance

- Fixed period: 10, 20, 25, or 30 years

- Coverage ends when term expires

- Best for: Temporary needs like mortgage protection, income replacement during working years, children’s education funding

Whole Life Insurance

- Lifetime coverage until death

- Never expires as long as premiums are paid

- Best for: Permanent needs like final expenses, estate planning, leaving a legacy, lifetime dependent care

Cash Value and Savings Component 💵

Term Life Insurance

- Zero cash value

- Pure protection only

- All premiums go toward insurance cost

- Nothing returned if you outlive the policy

Whole Life Insurance

- Builds cash value from year one

- Typical cash value at year 20: 40-60% of total premiums paid

- Can access through loans or withdrawals

- Surrender value available if you cancel the policy

Flexibility and Adaptability 🔧

Term Life Insurance

- High flexibility: Easy to adjust coverage as needs change

- Can ladder multiple policies (different terms ending at different times)

- Can convert to whole life (with convertible term)

- Simple to understand and manage

Whole Life Insurance

- Less flexible: Changing coverage requires policy amendments

- Long-term commitment required for value realization

- More complex to modify or adjust

- Requires ongoing premium payments regardless of changing circumstances

Tax Implications in Malaysia 🏛️

Both term and whole life insurance enjoy favorable tax treatment in Malaysia:

Premium Tax Relief

- Both qualify for personal income tax relief up to RM3,000 annually (as of 2026)

- This applies to premiums paid for self, spouse, and children

Death Benefit

- Completely tax-free for beneficiaries in both cases

- Not subject to estate duty (which Malaysia doesn’t have anyway)

Cash Value Growth (Whole Life)

- Grows tax-deferred

- No annual tax on accumulation

- Withdrawals and loans have specific tax treatments depending on circumstances

Term vs Whole Life Insurance in Malaysia: Which One Should You Choose?

Here’s the truth: there’s no universally “better” option. The right choice depends entirely on your unique situation, goals, and priorities.

Choose Term Life Insurance If You… 🎯

Have a Limited Budget If you’re earning RM3,000-6,000 monthly and need substantial coverage, term insurance is likely your only realistic option. RM100-150 per month can buy you RM1 million in protection—enough to truly secure your family’s future.

Have Temporary Financial Obligations

- You have a mortgage that will be paid off in 20-25 years

- Your children will complete their education in 15-20 years

- You’re supporting aging parents for a defined period

- You need income replacement only during your working years

Prefer to Invest Separately If you’re disciplined about investing and believe you can achieve better returns than the 3-5% offered by whole life cash values, the “buy term and invest the difference” strategy makes sense.

Need Maximum Coverage Now Young families with limited income but high protection needs (young children, large mortgage, single income) benefit most from term insurance’s high coverage at low cost.

Are in Your 20s-30s At this life stage, you typically need maximum protection at minimum cost. Term insurance delivers exactly that.

Choose Whole Life Insurance If You… 🎯

Want Lifetime Protection If you have permanent needs—a special needs child who will always depend on you, desire to leave a legacy, or want to ensure final expenses are covered—whole life provides certainty.

Struggle with Saving Discipline If you’ve tried saving independently but always end up spending the money, whole life’s forced savings mechanism might be worth the premium.

Have Estate Planning Goals High-net-worth individuals often use whole life insurance for:

- Equalizing inheritance among children

- Providing liquidity to pay estate settlement costs

- Creating a tax-free legacy

- Business succession planning

Can Comfortably Afford Higher Premiums If you’re earning RM10,000+ monthly and have already maximized other investment vehicles (EPF, unit trusts, stocks), whole life can serve as a diversification tool.

Want Guaranteed Wealth Accumulation If market volatility makes you anxious and you prefer the guaranteed (though modest) returns of whole life cash values, this might suit your risk profile.

Are in Your 40s-50s At this stage, term insurance becomes expensive, and you may have accumulated some wealth. Whole life can serve as a wealth preservation and transfer tool.

The Hybrid Approach: Why Not Both? 🤝

Here’s a strategy many financial planners recommend, and one I personally use: combine both types of insurance.

The Layering Strategy

Foundation Layer: Whole Life Purchase a smaller whole life policy (RM100,000-200,000) for:

- Permanent coverage for final expenses

- Cash value accumulation for emergencies

- Forced savings discipline

Protection Layer: Term Life Add substantial term coverage (RM500,000-1,000,000) for:

- High protection during peak earning and responsibility years

- Affordable premiums that free up cash for other investments

- Coverage that matches specific time-bound obligations

Real-Life Example: The Lim Family’s Hybrid Strategy

David Lim, 35, and his wife Mei Ling, 33, have two young children and a RM450,000 mortgage. Here’s their insurance strategy:

David’s Coverage:

- Whole life: RM150,000 (RM280/month)

- 25-year term: RM600,000 (RM110/month)

- Total coverage: RM750,000 for RM390/month

Mei Ling’s Coverage:

- Whole life: RM100,000 (RM180/month)

- 20-year term: RM400,000 (RM70/month)

- Total coverage: RM500,000 for RM250/month

Combined family premium: RM640/month

This strategy gives them:

- ✅ Substantial protection during their children’s dependent years

- ✅ Permanent coverage of RM250,000 that never expires

- ✅ Cash value accumulation in the whole life policies

- ✅ Affordable premiums that fit their RM12,000 monthly household income

- ✅ Flexibility to drop the term policies once their mortgage is paid and children are independent

Common Myths About Term vs Whole Life Insurance in Malaysia

Let me address some misconceptions I frequently encounter:

Myth #1: “Term Insurance is Wasted Money Because You Get Nothing Back”

Reality: This is like saying car insurance is wasted money if you don’t have an accident. Insurance is about transferring risk, not investment returns. Term insurance transfers the financial risk of your premature death to the insurer at the lowest cost. If you outlive the policy, that’s actually the best possible outcome—you’re alive and can continue earning!

Myth #2: “Whole Life Insurance is Always a Bad Investment”

Reality: While whole life typically underperforms direct equity investments, it’s not purely an investment—it’s insurance with a savings component. For people who lack savings discipline or want guaranteed, conservative growth with lifetime protection, it serves a valuable purpose. The “buy term and invest the difference” strategy only works if you actually invest the difference consistently.

Myth #3: “I Don’t Need Life Insurance Because I’m Single”

Reality: Even singles may need life insurance if they have:

- Aging parents who depend on their income

- Co-signed loans or business debts

- Desire to leave a legacy to siblings, nieces, nephews, or charities

- Final expenses they don’t want to burden family with

Myth #4: “My Company Insurance is Enough”

Reality: Group life insurance from employers typically provides only 1-2 times your annual salary—far less than the 10-15 times experts recommend. Plus, you lose this coverage if you change jobs or are laid off, often when you’re older and individual insurance is more expensive.

Myth #5: “I Can Always Buy Insurance Later When I Earn More”

Reality: Insurance gets significantly more expensive as you age. A 25-year-old pays roughly half what a 35-year-old pays for the same coverage. Plus, health issues that develop over time may make you uninsurable or subject to exclusions and higher premiums.

How to Calculate Your Life Insurance Needs in Malaysia

Before deciding between term and whole life, you need to know how much coverage you actually need. Here’s a practical framework:

The DIME Method 📊

D – Debt and Final Expenses Add up:

- Outstanding mortgage balance

- Car loans

- Personal loans

- Credit card debt

- Estimated funeral and final expenses (RM15,000-30,000)

I – Income Replacement Calculate how many years of income your family needs:

- Annual income × Number of years until retirement

- Alternatively: Annual income × 10-15 (rule of thumb)

M – Mortgage If not already counted in debt above, include the full outstanding balance

E – Education Estimate education costs for all children:

- Public university: RM40,000-60,000 per child

- Private university: RM100,000-200,000 per child

- Overseas education: RM300,000-500,000 per child

Example Calculation: Ahmad’s Coverage Needs

Ahmad, 32, earns RM6,000 monthly (RM72,000 annually):

- Debt: RM380,000 mortgage + RM45,000 car loan + RM20,000 final expenses = RM445,000

- Income: RM72,000 × 15 years = RM1,080,000

- Mortgage: Already counted above = RM0

- Education: 2 children × RM80,000 = RM160,000

Total coverage needed: RM1,685,000

Ahmad could achieve this with:

- 25-year term: RM1,500,000 (approximately RM200/month)

- Small whole life: RM200,000 (approximately RM350/month)

- Total: RM550/month for RM1,700,000 coverage

Or purely term:

- 25-year term: RM1,700,000 (approximately RM230/month)

The choice depends on whether Ahmad values the permanent coverage and cash value of the hybrid approach or prefers maximum affordability.

Factors That Affect Your Premiums in Malaysia

Understanding what influences your insurance costs helps you make informed decisions:

Age 👴👶

This is the single biggest factor. Insurance operates on mortality risk—the older you are, the higher the probability of death, and thus higher premiums. A 25-year-old might pay RM60/month for RM500,000 term coverage, while a 45-year-old pays RM180/month for the same coverage.

Gender 👨👩

Statistically, women live longer than men in Malaysia (average life expectancy: 78 for women vs. 74 for men). Therefore, women typically pay 10-20% less than men for the same coverage.

Smoking Status 🚬

Smokers pay dramatically higher premiums—typically 50-100% more than non-smokers. If you smoke a pack a day, your RM100/month premium might become RM150-200/month. This reflects the significantly higher health risks associated with smoking.

Health Condition 🏥

Pre-existing conditions affect premiums:

- Diabetes: 25-75% premium loading

- High blood pressure: 15-50% loading

- High cholesterol: 10-25% loading

- Obesity (BMI >30): 15-40% loading

- Previous cancer: May be declined or very high loading after remission period

Occupation 👷♂️

High-risk occupations face premium loadings:

- Construction workers

- Offshore oil rig workers

- Pilots

- Professional drivers

- Mining workers

Office workers and professionals typically get standard rates.

Lifestyle and Hobbies 🏂

Dangerous hobbies may result in exclusions or loadings:

- Scuba diving (beyond recreational depths)

- Rock climbing

- Skydiving

- Motor racing

- Aviation (private pilots)

Questions to Ask Before Buying Life Insurance in Malaysia

When comparing policies and meeting with insurance agents, ask these critical questions:

About the Policy 📋

“What exactly is guaranteed versus non-guaranteed in this illustration?”

- Whole life illustrations often show optimistic projections. Understand what’s contractually guaranteed.

“What is the surrender value at years 5, 10, 15, and 20?”

- If you need to cancel a whole life policy early, surrender values are often very low, sometimes less than total premiums paid.

“Can I convert this term policy to whole life later?”

- Convertibility is valuable if your needs change.

“What happens if I miss a premium payment?”

- Understand grace periods and policy lapse conditions.

“Are there any exclusions or waiting periods?”

- Suicide clauses (typically 1 year), pre-existing condition exclusions, etc.

About the Insurer 🏢

“What is your company’s claims settlement ratio?”

- Top insurers in Malaysia settle 95%+ of claims. Anything below 90% is concerning.

“What is your financial strength rating?”

- Look for insurers rated A or above by rating agencies like A.M. Best or Standard & Poor’s.

“How long does the typical claim take to process?”

- Reputable insurers process straightforward death claims within 7-14 days.

About Costs 💰

“What is the total premium I’ll pay over the policy lifetime?”

- For a 20-year term at RM100/month, you’ll pay RM24,000 total. For whole life at RM400/month for 30 years, that’s RM144,000.

“Are there any additional fees or charges?”

- Policy fees, administrative charges, fund management fees (for investment-linked policies).

“What is the effective cost per RM1,000 of coverage?”

- This helps compare policies with different structures.

The Investment-Linked Policy (ILP) Alternative

I should mention a third option that’s become increasingly popular in Malaysia: Investment-Linked Policies (ILPs). These combine insurance protection with investment in unit trust funds.

How ILPs Work

Your premium is split into:

- Insurance charges (cost of protection)

- Fund management fees

- Investment into selected funds (equity, bond, balanced, etc.)

The investment portion can grow based on fund performance, potentially offering higher returns than traditional whole life insurance.

ILP Advantages ✅

- Higher growth potential than whole life

- Flexibility to adjust coverage and investment allocation

- Transparency in charges and fund performance

- Can potentially achieve both protection and wealth growth

ILP Disadvantages ❌

- Investment risk: Your cash value can decrease if funds underperform

- Complex fee structures that can erode returns

- Requires active management and understanding of investments

- Protection cost increases with age, potentially consuming more of your premium over time

When to Consider ILPs

ILPs suit investors who:

- Understand investment risks and market volatility

- Want flexibility to adjust their coverage and investment mix

- Are comfortable with non-guaranteed returns

- Have a long investment horizon (15+ years)

However, many financial planners (myself included) often recommend keeping insurance and investment separate—buying term insurance for protection and investing directly in unit trusts or ETFs for wealth building. This typically offers better transparency, lower fees, and more flexibility.

Real Stories: How Malaysians Decided

Let me share a few more real-life examples (names changed for privacy) of how different Malaysians approached the term vs whole life insurance in Malaysia decision:

Case Study 1: The Young Professional

Profile: Sarah, 26, fresh graduate, RM3,500 monthly income, single, renting, no dependents but supporting parents occasionally.

Decision: 20-year term life insurance, RM300,000 coverage, RM50/month

Reasoning: Sarah needed affordable coverage in case something happened to her (her parents would lose her financial support). She chose term because:

- Her budget was tight

- She wanted to invest the difference in her EPF and unit trusts

- Her needs were temporary (until her parents retire and have their own savings)

- RM50/month was manageable; RM250/month for whole life wasn’t

Outcome: After 5 years, Sarah’s income had grown to RM6,500. She increased her term coverage to RM500,000 and started a small whole life policy (RM100,000) for permanent coverage.

Case Study 2: The Established Family

Profile: Kumar, 42, manager, RM12,000 monthly income, married, two children (ages 8 and 10), owns home with RM300,000 outstanding mortgage.

Decision: Hybrid approach

- Whole life: RM200,000 (RM520/month)

- 20-year term: RM600,000 (RM180/month)

- Total: RM800,000 coverage for RM700/month

Reasoning: Kumar wanted:

- Permanent coverage for final expenses and legacy (whole life)

- High protection during his children’s dependent years (term)

- Cash value accumulation for emergencies (whole life)

- Affordable total premium that fit his budget

Outcome: The strategy worked well. At age 50, Kumar’s whole life policy had accumulated RM85,000 in cash value. When his daughter needed unexpected medical treatment not fully covered by his health insurance, he borrowed RM40,000 from his policy at 4% interest, repaying it over 3 years.

Case Study 3: The Late Starter

Profile: Linda, 48, business owner, RM15,000 monthly income, divorced, one adult child (financially independent), no mortgage.

Decision: Whole life insurance, RM250,000 coverage, RM850/month

Reasoning: Linda had delayed getting life insurance. At 48:

- Term insurance was expensive (RM300+/month for RM500,000)

- She wanted permanent coverage, not just 10-15 years

- She had the budget for whole life premiums

- The cash value would supplement her retirement (EPF was modest due to years of self-employment)

- She wanted to leave a legacy for her grandchildren

Outcome: Linda views her whole life policy as a forced retirement savings plan that also provides a guaranteed inheritance for her family.

Making Your Decision: A Step-by-Step Framework

Here’s a practical framework to help you decide between term vs whole life insurance in Malaysia:

Step 1: Calculate Your Coverage Need 📊

Use the DIME method I outlined earlier. Be honest and comprehensive. Most Malaysians need RM500,000 to RM2,000,000 in coverage depending on their circumstances.

Step 2: Assess Your Budget 💵

Determine how much you can comfortably and sustainably allocate to insurance premiums monthly. A common guideline is 5-10% of your gross income.

For example:

- RM4,000 monthly income → RM200-400 for insurance

- RM6,000 monthly income → RM300-600 for insurance

- RM10,000 monthly income → RM500-1,000 for insurance

Step 3: Identify Your Primary Goal 🎯

Ask yourself: “What’s my main objective?”

If your answer is: “Maximum protection for my family at the lowest cost” → Choose term life insurance

If your answer is: “Lifetime coverage with built-in savings” → Choose whole life insurance

If your answer is: “Both protection and savings, and I can afford it” → Choose the hybrid approach

Step 4: Consider Your Life Stage 👨👩👧👦

Ages 20-35: Term insurance usually makes the most sense

- Premiums are very affordable

- You likely have high coverage needs but limited budget

- You have time to build wealth through other investments

Ages 35-50: Hybrid approach often works best

- You can afford higher premiums

- You want permanent coverage plus high temporary protection

- Cash value provides financial flexibility

Ages 50+: Whole life becomes more attractive

- Term insurance is expensive at this age

- You’re thinking about legacy and estate planning

- You may have accumulated wealth and need less pure protection

Step 5: Evaluate Your Savings Discipline 💪

Be brutally honest: If you buy term and “invest the difference,” will you actually invest the difference consistently?

If yes → Term + separate investments may yield better results If no → Whole life’s forced savings might be worth the lower returns

Step 6: Get Multiple Quotes 📝

Don’t buy from the first agent you meet. Get quotes from at least 3-4 insurers:

- Prudential

- Great Eastern

- AIA

- Allianz

- Manulife

- Tokio Marine

Premiums can vary 20-30% for similar coverage.

Step 7: Read the Fine Print 🔍

Before signing:

- Review all exclusions and waiting periods

- Understand the claims process

- Verify the surrender values (for whole life)

- Confirm the renewal terms (for term)

- Check the free-look period (typically 15 days to cancel without penalty)

Common Mistakes to Avoid

Through years of observing friends, family, and clients navigate insurance decisions, I’ve seen these mistakes repeatedly:

❌ Mistake #1: Buying Too Little Coverage to Afford Whole Life

Many people buy RM100,000-200,000 whole life policies when they actually need RM800,000-1,000,000 in coverage. They’re underinsured because they prioritized the savings component over adequate protection.

Better approach: Buy sufficient term coverage first, then add whole life if budget allows.

❌ Mistake #2: Letting Policies Lapse

Life gets busy, finances get tight, and people let policies lapse—especially whole life policies where they’ve paid for years. Surrendering a whole life policy early often means getting back less than you paid in premiums.

Better approach: Buy only what you can sustain long-term. Better to have RM300,000 term coverage you maintain than RM500,000 whole life you cancel after 5 years.

❌ Mistake #3: Relying Solely on Employer Coverage

Group life insurance is a great benefit but shouldn’t be your only coverage. You lose it when you change jobs, and it’s typically insufficient.

Better approach: Get your own individual policy. Treat employer coverage as a bonus, not your foundation.

❌ Mistake #4: Buying Based on Agent Relationship Rather Than Needs

Your neighbor’s cousin who just became an insurance agent is lovely, but that doesn’t mean their recommended product is right for you.

Better approach: Evaluate products objectively. A good agent will recommend what’s best for you, not what earns them the highest commission.

❌ Mistake #5: Not Reviewing Coverage Regularly

Your RM300,000 policy made sense at 25. At 35 with two kids and a mortgage, it’s woefully inadequate.

Better approach: Review your coverage every 3-5 years or after major life events (marriage, children, home purchase, income increase).

❌ Mistake #6: Focusing Only on Returns

Some people reject whole life because “the returns are only 3-4%.” But insurance isn’t purely an investment—it’s risk transfer with a savings component.

Better approach: Evaluate insurance primarily on protection value, secondarily on cash value accumulation.

The Future of Life Insurance in Malaysia (2026 and Beyond)

The insurance landscape is evolving rapidly. Here are trends shaping the term vs whole life insurance in Malaysia landscape:

Digital Distribution 📱

More insurers are offering online term life insurance with:

- Instant approval for standard cases

- No medical examination for coverage up to RM500,000 (for young, healthy applicants)

- Lower premiums due to reduced distribution costs

- Fully digital claims submission

Companies like PolicyStreet, Etiqa, and FWD are leading this digital transformation.

Personalized Pricing 📊

Insurers are increasingly using data analytics to offer personalized premiums based on:

- Wearable device data (fitness trackers)

- Lifestyle choices

- Genetic testing (still emerging and controversial)

This could mean lower premiums for healthy, active individuals.

Hybrid Products 🔄

New products blur the line between term and whole life:

- Term policies with return of premium (ROP) riders

- Whole life with flexible premium payments

- Modular policies where you can adjust components

Sustainability and ESG Integration 🌱

Some insurers now offer premium discounts for:

- Electric vehicle owners

- Sustainable lifestyle choices

- Regular health check-ups

This trend will likely accelerate.

Frequently Asked Questions

Q: Can I have both term and whole life insurance?

Absolutely! In fact, many financial planners recommend this hybrid approach. You get maximum protection from affordable term insurance during your peak responsibility years, plus permanent coverage and cash value accumulation from a smaller whole life policy.

Q: What happens if I can’t afford my whole life premiums anymore?

You have several options:

- Use accumulated cash value to pay premiums (if sufficient)

- Reduce the coverage amount to lower premiums

- Convert to a paid-up policy (lower coverage, no more premiums required)

- Surrender the policy and receive the cash value (minus surrender charges)

Q: Is term life insurance really “wasted” if I outlive the policy?

No. The purpose of insurance is to transfer risk. If you outlive your term policy, that’s the best possible outcome—you’re alive and healthy! The premiums paid provided peace of mind and protection when you needed it most. It’s like saying car insurance is wasted if you don’t have an accident.

Q: Can I convert my term policy to whole life later?

Many term policies include a conversion option, allowing you to convert to whole life within a specified period (often 5-10 years) without medical underwriting. This is valuable if your health deteriorates or your needs change. Check if your policy includes this feature.

Q: How do I know if an insurance company is reliable?

Check:

- Claims settlement ratio (should be 95%+)

- Financial strength ratings from agencies like A.M. Best

- Years in operation in Malaysia

- Customer reviews and complaints

- Licensing by Bank Negara Malaysia

Top-rated insurers in Malaysia include Prudential, Great Eastern, AIA, and Allianz.

Q: Should I get insurance from a bank or an insurance company?

Both are legitimate channels. Banks often sell insurance products (bancassurance), which can be convenient. However:

- Compare products across multiple providers

- Ensure the product meets your needs, not just the seller’s targets

- Understand all fees and charges

- Don’t feel pressured to buy insurance just because you’re getting a loan

Q: What’s the difference between life insurance and takaful?

Takaful is the Islamic alternative to conventional insurance, based on mutual cooperation and shared responsibility. The fundamental difference:

- Insurance: Risk transfer to an insurance company

- Takaful: Risk sharing among participants

Both offer term and whole life (called “family takaful”) options. Choose based on your religious preferences and product features.

Taking Action: Your Next Steps

You’ve made it through this comprehensive guide on term vs whole life insurance in Malaysia. Now it’s time to take action. Here’s your roadmap:

Immediate Actions (This Week) ✅

- Calculate your coverage needs using the DIME method

- Assess your budget for insurance premiums (5-10% of income)

- List your priorities: maximum protection, savings component, legacy planning, etc.

- Research 3-4 reputable insurers in Malaysia

Short-term Actions (This Month) ✅

- Request quotes from multiple insurers for both term and whole life

- Meet with 2-3 licensed agents or financial advisors (get different perspectives)

- Compare proposals side-by-side, focusing on:

- Total coverage amount

- Monthly premium

- Guaranteed vs. non-guaranteed benefits

- Exclusions and limitations

- Insurer’s reputation and claims ratio

- Ask all your questions before making a decision

Long-term Actions (Ongoing) ✅

- Purchase your policy once you’re confident in your choice

- Keep all policy documents in a safe, accessible place

- Inform your beneficiaries about your coverage

- Review your coverage every 3-5 years or after major life events

- Maintain your premiums consistently—don’t let policies lapse

- Update beneficiaries as your life circumstances change

Conclusion: The Best Insurance is the One You Have

After exploring every angle of the term vs whole life insurance in Malaysia debate, here’s my final perspective: The best insurance policy is the one you actually purchase and maintain.

I’ve seen too many people paralyzed by analysis, endlessly comparing term versus whole life, waiting for the “perfect” policy, only to remain uninsured for years. Meanwhile, life happens—accidents, illnesses, unexpected deaths—and families are left financially devastated.

For most Malaysians, especially those in their 20s-40s, term life insurance is the right starting point. It provides maximum protection at minimum cost when your family needs it most. You can always add whole life coverage later as your income grows and your needs evolve.

For those who can afford it and value the forced savings and permanent coverage, whole life insurance serves an important purpose. It’s not just about returns—it’s about guaranteed protection, disciplined wealth accumulation, and legacy planning.

And for many, the hybrid approach offers the best of both worlds—substantial term coverage for current needs plus a foundation of permanent whole life protection.

Whatever you choose, make the choice now. Get covered today. Your family’s financial security depends not on having the theoretically optimal policy, but on having adequate protection in place when the unexpected happens.

Remember Ahmad from the beginning of this article? After his father’s death, he didn’t just grieve—he took action. Within two weeks, he purchased a 25-year term policy with RM800,000 coverage for RM140 per month. He also convinced his siblings to get covered. “I never want my family to face what we went through,” he told me.

That’s the power of life insurance—not the policy type you choose, but the protection you provide and the peace of mind you create.

Now it’s your turn. Calculate your needs, compare your options, and take action. Your family’s future is worth it.