Imagine this: You’re sitting in a hospital waiting room, watching the bill climb higher with every test and consultation. Your heart races — not because of the diagnosis, but because you’re not sure your insurance will cover it. This is the reality for millions of Malaysians in 2026, and it’s exactly why understanding the difference between Medical Health Insurance Takaful (MHIT) vs Investment-Linked Insurance in Malaysia 2026 has never been more important.

I’ve spent years helping people navigate the confusing world of insurance and takaful in Malaysia. And if there’s one thing I’ve learned, it’s this: choosing the wrong type of coverage can cost you tens of thousands of ringgit — or worse, leave you unprotected when you need it most.

With Bank Negara Malaysia (BNM) officially announcing the pilot implementation of the standardised base MHIT plan in the second half of 2026, the insurance landscape in Malaysia is undergoing a historic transformation. Whether you’re a first-time buyer or someone looking to review your existing coverage, this guide will walk you through everything you need to know about Medical Health Insurance Takaful (MHIT) vs Investment-Linked Insurance in Malaysia 2026 — in plain, simple language.

Let’s dive in. 🚀

Key Takeaways 📋

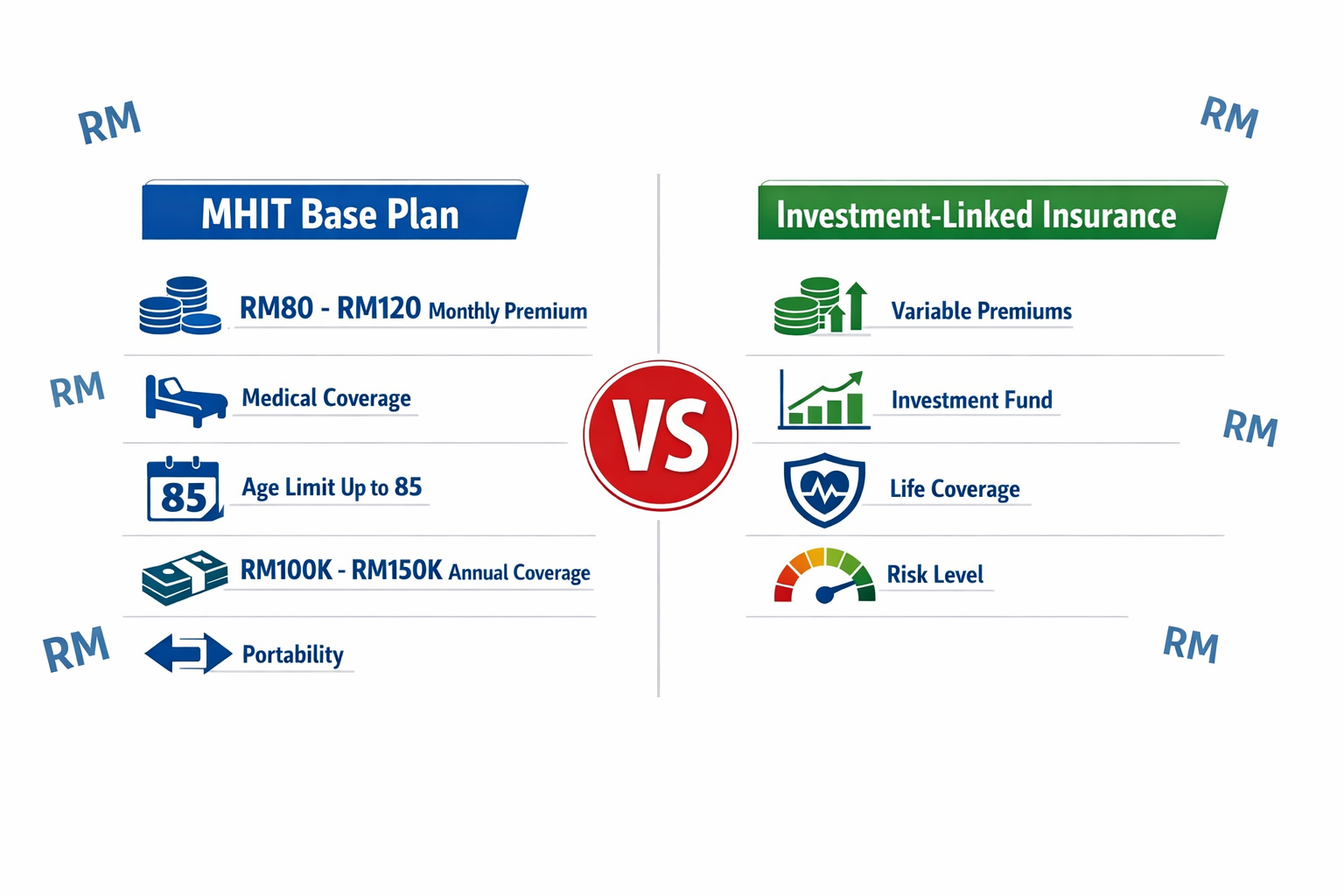

- The base MHIT plan is a standardised medical and health insurance/takaful product launching in pilot form in H2 2026, with monthly premiums estimated between RM80 and RM120, offering up to RM150,000 in annual coverage with no lifetime limit.

- Investment-linked insurance (ILP) combines life protection with an investment component, but the investment risk falls on you, the policyholder — not the insurer.

- MHIT focuses purely on medical coverage, while investment-linked policies bundle medical riders with savings/investment features, which can make them more expensive and complex.

- The new MHIT plan introduces seamless portability — you can switch between insurers or takaful operators without undergoing new medical checks.

- You don’t have to choose just one. Many Malaysians in 2026 will benefit from a combination of both products, depending on their life stage, health needs, and financial goals.

Understanding the Malaysian Insurance Landscape in 2026

Before we compare MHIT and investment-linked insurance head-to-head, let’s set the stage. Malaysia’s insurance and takaful industry has been evolving rapidly, driven by regulatory changes, rising healthcare costs, and shifting consumer expectations.

Why Is This Conversation Happening Now?

Healthcare costs in Malaysia have been rising at an average rate of 10% to 15% annually over the past decade. Private hospital bills that once seemed manageable are now eye-watering. A simple appendectomy that cost RM8,000 a decade ago can now run you RM15,000 or more.

At the same time, many Malaysians have found themselves trapped in insurance products they don’t fully understand. Some bought investment-linked policies thinking they were getting comprehensive medical coverage, only to discover — sometimes during a medical emergency — that their coverage had eroded because the investment component underperformed.

“The base MHIT plan serves as a complement to healthcare access, not a replacement for public healthcare, and will establish a benchmark for market improvements.”

— Finance Minister II Amir Hamzah Azizan, January 22, 2026

This statement is crucial. It tells us that the government sees MHIT as a foundational layer of protection — something every Malaysian should have access to, regardless of income level.

The Regulatory Push

Bank Negara Malaysia has been working behind the scenes for years to address the affordability and sustainability crisis in medical insurance. The announcement on January 21-22, 2026, confirmed that:

- A standardised base MHIT plan will undergo pilot implementation in H2 2026

- Full rollout is targeted for early 2027

- BNM will strengthen regulatory requirements for all MHIT products

- The framework aims to improve consumer protection and ensure long-term premium sustainability

This is a game-changer. For the first time, there will be a government-backed benchmark that all insurers and takaful operators must measure up to.

What Is Medical Health Insurance Takaful (MHIT)? A Deep Dive

The Basics of MHIT

Medical Health Insurance Takaful — or MHIT — is the umbrella term used by Bank Negara Malaysia to describe medical and health insurance products (conventional) and takaful plans (Islamic). The term covers both conventional insurance and Shariah-compliant takaful products.

Think of MHIT as a pure medical protection product. Its sole purpose is to cover your medical and hospitalisation expenses. There’s no investment component, no savings element — just straightforward medical coverage.

The New Base MHIT Plan: What We Know

Here’s a breakdown of the confirmed features of the standardised base MHIT plan launching in 2026:

| Feature | Details |

|---|---|

| Monthly Premium | RM80 – RM120 |

| Annual Coverage Limit (Age ≤ 60) | RM100,000 |

| Annual Coverage Limit (Age > 60) | RM150,000 |

| Lifetime Limit | ❌ None (annual caps only) |

| Maximum Coverage Age | Up to 85 years old |

| Maximum Enrollment Age | 70 years old |

| Portability | ✅ Seamless switching between providers |

| Medical Underwriting for Switching | ❌ Not required |

| Pilot Launch | H2 2026 |

| Full Rollout | Early 2027 |

| Feature | Details |

|---|---|

| Monthly Premium | RM80 – RM120 |

| Annual Coverage Limit (Age ≤ 60) | RM100,000 |

| Annual Coverage Limit (Age > 60) | RM150,000 |

| Lifetime Limit | ❌ None (annual caps only) |

| Maximum Coverage Age | Up to 85 years old |

| Maximum Enrollment Age | 70 years old |

| Portability | ✅ Seamless switching between providers |

| Medical Underwriting for Switching | ❌ Not required |

| Pilot Launch | H2 2026 |

| Full Rollout | Early 2027 |

Why the Base MHIT Plan Matters

Let me share a quick story. A friend of mine — let’s call him Razak — bought an investment-linked policy in his late 20s. He was told it would cover his medical needs and grow his money at the same time. Fast forward 15 years: the investment portion had barely grown due to market downturns and high fund management fees, and his medical rider premiums had skyrocketed. At 43, he was paying over RM500 a month and his actual medical coverage was less than what the new base MHIT plan offers for RM80-RM120.

Razak’s story isn’t unique. It’s why the base MHIT plan is so significant:

- Affordability: At RM80-RM120 per month, it’s accessible to the B40 and M40 income groups

- Transparency: Standardised benefits mean no hidden surprises

- Portability: If you’re unhappy with your provider, you can switch without penalty or new medical checks

- No Lifetime Cap: You won’t “run out” of coverage over your lifetime — only annual limits apply

- Senior-Friendly: Coverage extends to age 85, with higher annual limits for those over 60

💡 Pro Tip: The higher annual limit of RM150,000 for seniors above 60 reflects the reality that healthcare costs tend to increase significantly as we age. This is a thoughtful design feature.

MHIT vs Traditional Medical Cards

Many Malaysians are familiar with “medical cards” — the plastic cards issued by insurers that allow cashless admission to panel hospitals. The base MHIT plan will function similarly but with standardised terms and conditions across all providers.

Currently, medical card products vary wildly between companies. One insurer might cover a particular treatment while another excludes it. The base MHIT plan aims to eliminate this confusion by creating a uniform baseline that all providers must offer.

What Is Investment-Linked Insurance? Understanding the Other Side

How Investment-Linked Policies (ILPs) Work

Investment-linked insurance is a hybrid product that combines life insurance protection with an investment component. When you pay your premium, a portion goes toward your insurance coverage (including any medical riders), and the rest is invested in unit trust funds of your choice.

Here’s a simplified breakdown:

<code>Your Monthly Premium

├── Insurance Charges (mortality, medical rider, admin fees)

└── Investment Units (allocated to chosen funds)

</code>The appeal is obvious: you get protection and your money grows. But as with most things that sound too good to be true, there are important caveats.

The Investment Risk Falls on You 🎯

This is perhaps the single most important thing to understand about investment-linked insurance. Unlike traditional whole-life or endowment policies where the insurer bears the investment risk, ILPs transfer that risk entirely to the policyholder.

Financial advisor Phang Kar Yew of GV Wealth Planners has noted that investment-linked policies are increasingly preferred by insurers precisely because they shift investment risk to policyholders while reducing insurer liability. This isn’t necessarily a bad thing — but you need to go in with your eyes open.

Why Insurers Love ILPs

From the insurer’s perspective, ILPs are attractive for several reasons:

- Reduced Capital Requirements: Under the Risk-Based Capital (RBC) framework, insurers need adequate capital reserves. ILPs reduce this burden because the investment risk sits with the policyholder.

- Fee Income: Fund management fees, policy administration charges, and switching fees create steady revenue streams.

- Flexibility Marketing: ILPs can be marketed as “all-in-one” solutions, which appeals to consumers who want simplicity.

As financial advisor Derick KK Tan of Great Vision Financial Advisory has pointed out, the RBC framework implementation has accelerated the shift toward investment-linked products across the Malaysian insurance industry.

The Anatomy of ILP Charges

Let’s break down what you’re actually paying for in a typical investment-linked policy:

| Charge Type | Description | Impact |

|---|---|---|

| Premium Allocation Charge | Percentage deducted before investment | Reduces your invested amount (especially high in early years) |

| Fund Management Fee | Annual fee for managing investment funds | Typically 0.5% – 1.5% of fund value |

| Insurance Charges | Cost of your life and medical coverage | Increases with age |

| Policy Administration Fee | Monthly/annual admin charge | Fixed amount deducted regularly |

| Surrender Charge | Penalty for early termination | Can be significant in first 5-10 years |

| Switching Fee | Fee for changing investment funds | May be free for limited switches per year |

⚠️ Warning: In the early years of an ILP, premium allocation charges can be as high as 60-80% of your premium. This means if you pay RM300/month, only RM60-RM120 might actually be invested in the first few years. The rest goes to charges and commissions.

Medical Health Insurance Takaful (MHIT) vs Investment-Linked Insurance in Malaysia 2026: The Head-to-Head Comparison

Now let’s get to the heart of the matter. Here’s a comprehensive comparison to help you understand exactly how these two products stack up against each other in 2026.

Purpose and Design Philosophy

MHIT (Base Plan):

- 🎯 Single purpose: Medical and hospitalisation coverage

- Designed for affordability and accessibility

- Standardised benefits across all providers

- Government-regulated benchmark product

Investment-Linked Insurance:

- 🎯 Dual purpose: Life protection + investment growth

- Designed for wealth accumulation alongside protection

- Benefits vary significantly between providers and plans

- Market-driven product with regulatory oversight

Cost Comparison

This is where things get really interesting. Let’s compare the costs for a 35-year-old non-smoker in Malaysia:

| Factor | Base MHIT Plan | Investment-Linked Policy (with Medical Rider) |

|---|---|---|

| Monthly Premium | RM80 – RM120 | RM250 – RM800+ |

| Premium Stability | Designed for long-term sustainability | Can increase significantly with age |

| What You Pay For | 100% goes to medical coverage | Split between insurance charges + investment |

| Hidden Costs | Minimal (standardised) | Fund management fees, allocation charges, admin fees |

| 10-Year Total Cost | ~RM9,600 – RM14,400 | ~RM30,000 – RM96,000+ |

📊 The math is clear: If your primary concern is medical coverage, the base MHIT plan offers significantly better value per ringgit spent on healthcare protection.

Coverage Comparison

| Coverage Aspect | Base MHIT Plan | Investment-Linked (Medical Rider) |

|---|---|---|

| Annual Limit | RM100K (≤60) / RM150K (>60) | Varies: RM50K – Unlimited |

| Lifetime Limit | None ✅ | Often capped (RM500K – RM2M) |

| Room & Board | Standardised | Varies by plan tier |

| Outpatient Coverage | TBD (pilot phase) | Usually limited or add-on |

| Coverage Age | Up to 85 | Typically up to 80-100 (varies) |

| Life Coverage | ❌ Not included | ✅ Included |

| Critical Illness | ❌ Not included | ✅ Often included as rider |

| Investment Returns | ❌ Not applicable | ✅ Potential growth (with risk) |

Portability and Flexibility

One of the most revolutionary features of the base MHIT plan is its seamless portability. Here’s what this means in practice:

MHIT Portability ✅:

- Switch between insurers/takaful operators freely

- No new medical underwriting required

- No penalty for switching

- Your coverage continues uninterrupted

- Pre-existing conditions remain covered after switching

ILP Portability ⚠️:

- Switching providers typically means starting a new policy

- New medical underwriting is usually required

- Pre-existing conditions may be excluded under the new policy

- Surrender charges may apply if you cancel early

- Loss of accumulated no-claim benefits

Let me put this in perspective with another story. My colleague Sarah wanted to switch her ILP from Company A to Company B because Company B offered better fund options. But during the medical underwriting for the new policy, a minor health issue she’d developed since buying her original policy was flagged. Company B either wanted to exclude that condition or charge a higher premium. Sarah was stuck — she couldn’t move without losing coverage for a condition she was already covered for.

With the base MHIT plan, Sarah’s problem simply wouldn’t exist. 🎉

Medical Health Insurance Takaful (MHIT) vs Investment-Linked Insurance in Malaysia 2026: Who Should Choose What?

MHIT Is Ideal For:

✅ Budget-conscious individuals and families — If you’re in the B40 or M40 income group, the RM80-RM120 monthly premium is designed with you in mind.

✅ People who want pure medical protection — If you already have separate investment vehicles (EPF, ASB, unit trusts, stocks), you don’t need your insurance to double as an investment.

✅ Self-employed and gig workers — Without employer-provided medical benefits, the base MHIT plan offers an affordable safety net.

✅ Seniors and near-retirees — Coverage up to age 85 with higher annual limits for those over 60 makes this particularly attractive for older Malaysians.

✅ People who value simplicity — No investment decisions to make, no fund performance to monitor, no complex charge structures to decipher.

Investment-Linked Insurance Is Ideal For:

✅ Those who want life coverage + medical coverage in one product — If you need both life insurance and medical coverage and prefer a single policy, ILPs offer convenience.

✅ Higher-income individuals seeking larger coverage — If RM100,000-RM150,000 annual medical coverage isn’t enough (e.g., you want private hospital coverage with no annual limit), premium ILP medical riders can offer more.

✅ Disciplined investors who understand the product — If you genuinely understand how ILPs work, are comfortable with investment risk, and have a long time horizon, the investment component can add value.

✅ Those who need critical illness and disability coverage — ILPs can bundle multiple types of coverage under one policy, which some people prefer for simplicity.

✅ Young professionals starting their financial journey — For someone in their 20s with decades of compounding ahead, the investment component of an ILP can grow meaningfully — if the right funds are chosen and fees are managed.

The Hybrid Approach: Why Not Both? 🤝

Here’s what I recommend to most people I advise: consider using both products strategically.

Strategy Example for a 35-year-old Malaysian earning RM5,000/month:

| Product | Purpose | Monthly Cost |

|---|---|---|

| Base MHIT Plan | Core medical coverage (RM100K annual) | ~RM100 |

| Investment-Linked Policy | Life coverage (RM500K) + top-up medical rider + investment | ~RM300 |

| Total | Comprehensive protection + wealth building | ~RM400 |

This hybrid approach gives you:

- Affordable base medical coverage that’s portable and sustainable

- Additional medical coverage for higher-end treatments if needed

- Life insurance protection for your dependents

- Investment growth potential for long-term wealth building

- Redundancy — if one policy lapses, you still have the other

Common Misconceptions About MHIT and Investment-Linked Insurance

Misconception #1: “MHIT Will Replace My Existing Medical Card”

Reality: The base MHIT plan is designed to be a floor, not a ceiling. It establishes a minimum standard of coverage. If your existing medical card offers better benefits, you can keep it. However, the MHIT framework will push all insurers to improve their offerings.

Misconception #2: “Investment-Linked Insurance Is a Scam”

Reality: ILPs are legitimate financial products regulated by BNM. The problem isn’t the product itself — it’s the mis-selling and lack of understanding. When properly explained and appropriately sold, ILPs can serve a valid purpose in your financial plan. The issue arises when agents sell ILPs as “savings plans” without adequately explaining the risks and charges.

Misconception #3: “The RM100,000 Annual Limit Is Too Low”

Reality: For the majority of medical situations in Malaysia, RM100,000 per year is sufficient. According to industry data, the average hospitalisation claim in Malaysia is between RM5,000 and RM20,000. Even major surgeries like heart bypass or cancer treatment typically fall within the RM50,000-RM100,000 range at private hospitals. The RM150,000 limit for seniors over 60 provides additional headroom.

However, if you frequently use premium private hospitals or anticipate needing cutting-edge treatments, you may want supplementary coverage.

Misconception #4: “I’m Young and Healthy — I Don’t Need Medical Insurance”

Reality: This is perhaps the most dangerous misconception. Accidents don’t discriminate by age. Cancer can strike at 25. The best time to buy medical coverage is when you’re young and healthy because:

- Premiums are lower

- No pre-existing conditions to worry about

- You lock in coverage before health issues develop

Misconception #5: “Takaful and Conventional Insurance Are Basically the Same”

Reality: While they serve similar purposes, the underlying structures differ significantly:

| Aspect | Conventional Insurance | Takaful |

|---|---|---|

| Concept | Risk transfer (you pay, insurer bears risk) | Risk sharing (mutual assistance among participants) |

| Shariah Compliance | Not required | Fully Shariah-compliant |

| Surplus/Profit | Belongs to the insurer | Shared between participants and operator |

| Investment | May include non-Shariah instruments | Only Shariah-compliant investments |

| Governance | Standard corporate governance | Additional Shariah committee oversight |

The base MHIT plan will be available in both conventional and takaful versions, so you can choose based on your preference.

How the RBC Framework Is Shaping Insurance in Malaysia

Understanding the Risk-Based Capital (RBC) framework helps explain why the insurance landscape looks the way it does in 2026.

The RBC framework requires insurers to hold capital reserves proportional to the risks they take on. Traditional guaranteed products (like whole-life policies with guaranteed cash values) require insurers to hold more capital because they bear the investment risk.

Investment-linked products, on the other hand, require less capital from insurers because the investment risk is transferred to policyholders. This is a key reason why the industry has shifted so dramatically toward ILPs over the past decade.

What this means for you:

- Fewer traditional guaranteed medical insurance products are available

- ILPs dominate the market because they’re more capital-efficient for insurers

- The base MHIT plan represents the government’s effort to ensure affordable, standardised medical coverage exists despite this market shift

Practical Steps: How to Evaluate Your Insurance Needs in 2026

Step 1: Assess Your Current Coverage 📋

Pull out all your existing insurance and takaful policies. For each one, note:

- Type of product (MHIT, ILP, term life, etc.)

- Monthly/annual premium

- Medical coverage limits (annual and lifetime)

- Life coverage amount

- Riders attached

- Current cash value (for ILPs)

- Premium payment term remaining

Step 2: Calculate Your Protection Gap

Ask yourself these questions:

- If I’m hospitalised tomorrow, how much would my policies cover?

- If I pass away, would my family be financially secure?

- If I’m diagnosed with a critical illness, can I afford treatment and living expenses?

- Am I paying for coverage I don’t need?

- Am I under-covered in any area?

Step 3: Consider the Base MHIT Plan

Once the pilot launches in H2 2026, evaluate whether the base MHIT plan should be your foundation. For most Malaysians, the answer will be yes. At RM80-RM120/month, it’s one of the most cost-effective ways to secure medical coverage.

Step 4: Decide on Supplementary Coverage

If the base MHIT plan’s RM100,000-RM150,000 annual limit isn’t sufficient for your needs, consider:

- A standalone medical insurance/takaful plan with higher limits

- An ILP with a comprehensive medical rider

- A standalone critical illness policy

Step 5: Separate Protection from Investment

This is my strongest piece of advice: don’t rely on your insurance policy as your primary investment vehicle. The fees in ILPs are typically higher than investing directly in unit trusts or ETFs. Consider:

| Need | Best Product |

|---|---|

| Medical coverage | Base MHIT plan + supplementary medical if needed |

| Life coverage | Term life insurance (cheapest) or ILP |

| Investment/savings | EPF, PRS, unit trusts, ASB, stocks, ETFs |

| Critical illness | Standalone CI policy or rider |

Step 6: Review Annually 🔄

Your insurance needs change as your life changes. Review your coverage every year, especially after:

- Getting married

- Having children

- Buying a home

- Changing jobs

- Receiving a significant salary increase

- Reaching milestone ages (30, 40, 50, 60)

What to Expect from the MHIT Pilot in H2 2026

As we approach the pilot implementation, here’s what you should watch for:

Timeline

- H2 2026: Pilot implementation begins with selected insurers and takaful operators

- Early 2027: Full market rollout targeted

How to Prepare

- Stay informed: Follow BNM announcements and your insurer’s communications

- Don’t rush to cancel existing policies: Wait until the base MHIT plan is officially available and you can compare terms

- Consult a licensed financial advisor: Get personalised advice based on your specific situation

- Budget for it: Start setting aside RM100-RM120/month now so you’re ready when the plan launches

Questions to Ask Your Insurance Agent

When discussing Medical Health Insurance Takaful (MHIT) vs Investment-Linked Insurance in Malaysia 2026 with your agent, ask:

- “How does the new base MHIT plan compare to my current medical coverage?”

- “What percentage of my ILP premium actually goes toward medical coverage vs. investment?”

- “What happens to my medical coverage if my ILP investment performs poorly?”

- “Can I keep my existing policy AND add the base MHIT plan?”

- “What are the total charges I’m paying in my ILP, including all hidden fees?”

- “If I switch to the base MHIT plan, will I lose any coverage for pre-existing conditions?”

The Future of Insurance in Malaysia: Beyond 2026

The introduction of the base MHIT plan is just the beginning. Here’s what I expect to see in the coming years:

Greater Transparency

BNM’s regulatory push will force all insurers and takaful operators to be more transparent about charges, coverage terms, and premium sustainability. This is a win for consumers.

Digital-First Experiences

Expect more insurers to offer fully digital enrollment, claims processing, and policy management. The portability feature of the base MHIT plan will likely be facilitated through a centralised digital platform.

Competitive Pricing Pressure

With a government-backed benchmark at RM80-RM120/month, existing MHIT products will face pressure to either lower prices or significantly improve benefits to justify higher premiums.

Evolution of ILPs

Investment-linked products won’t disappear, but they’ll need to evolve. Expect:

- Lower fee structures

- Better fund performance transparency

- Clearer separation of insurance and investment components

- More flexible premium allocation options

Health Ecosystem Integration

The future likely includes integration between MHIT plans and broader health initiatives — preventive care incentives, wellness programs, telemedicine, and chronic disease management.

Conclusion: Making Your Decision with Confidence ✅

The debate around Medical Health Insurance Takaful (MHIT) vs Investment-Linked Insurance in Malaysia 2026 isn’t about declaring one product “better” than the other. It’s about understanding what each product does, who it’s designed for, and how it fits into your unique financial picture.

Here’s my bottom line:

If you need affordable, straightforward medical coverage → The base MHIT plan (launching H2 2026) should be your starting point. At RM80-RM120/month with no lifetime limit and seamless portability, it’s a landmark product for Malaysian consumers.

If you need comprehensive protection including life coverage, critical illness, and investment → An investment-linked policy can serve as a powerful all-in-one tool — but only if you understand the charges, accept the investment risk, and choose your funds wisely.

For most Malaysians, the smartest approach is a combination: Use the base MHIT plan as your medical coverage foundation, and supplement with other products (ILP, term life, standalone critical illness) based on your specific needs and budget.

Your Action Steps for 2026:

- 📋 Audit your current coverage — Know exactly what you have and what you’re paying

- 💰 Budget RM100-RM120/month for the base MHIT plan when it launches

- 📞 Schedule a meeting with a licensed, independent financial advisor (not just an agent tied to one company)

- 📚 Educate yourself — Read BNM’s official announcements as the pilot progresses

- ⏰ Don’t wait — If you’re currently uninsured, get basic coverage NOW. You can always adjust when the base MHIT plan becomes available

The best insurance decision is an informed one. And now, you have the information you need to make it.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Insurance and takaful products are regulated by Bank Negara Malaysia. Always consult a licensed financial advisor before making insurance decisions. Product details mentioned are based on publicly announced information as of early 2026 and may be subject to change during the pilot and rollout phases.